You have the absolute legal right to stop a payday lender from draining your bank account. Even if you previously signed a contract giving them access, that permission isn't permanent. It's frustrating to watch your balance drop to zero because of aggressive withdrawals, leaving you without enough money for rent or basic groceries. You're likely tired of the cycle of overdraft fees and the stress of constant lender communication. We understand the urgency of your situation and the need for immediate relief.

This guide provides the exact steps for stopping automatic payments on a payday loan so you can regain control of your cash flow today. You'll learn how to exercise your federal rights to revoke ACH authorization and protect your remaining funds. We will walk you through the tactical process of notifying your bank, managing stop payment fees which typically range from $20 to $35, and finding a more manageable loan alternative. Follow these instructions to secure your account and stop the next scheduled debit before it happens.

Key Takeaways

- Federal law provides a clear legal shield to halt recurring electronic withdrawals from your account. Learn how to exercise your rights under the Electronic Fund Transfer Act to protect your cash flow.

- Follow a proven two-step tactical plan for stopping automatic payments on a payday loan by notifying both your lender and your financial institution. Act now to prevent the next scheduled debit from depleting your funds.

- Issue a formal stop-payment order to your bank to block specific unauthorized transactions immediately. This step is crucial for securing money needed for essential living expenses like rent and groceries.

- Understand how to manage lender communication and navigate the fallout after you revoke payment authorization. Gain the tools to handle aggressive collection attempts while maintaining a professional distance.

- Explore sustainable alternatives like installment loans to replace unmanageable high-interest debt. Discover how to transition to a more predictable payment structure that fits your current budget.

Understanding Your Legal Right to Stop Automatic Debits

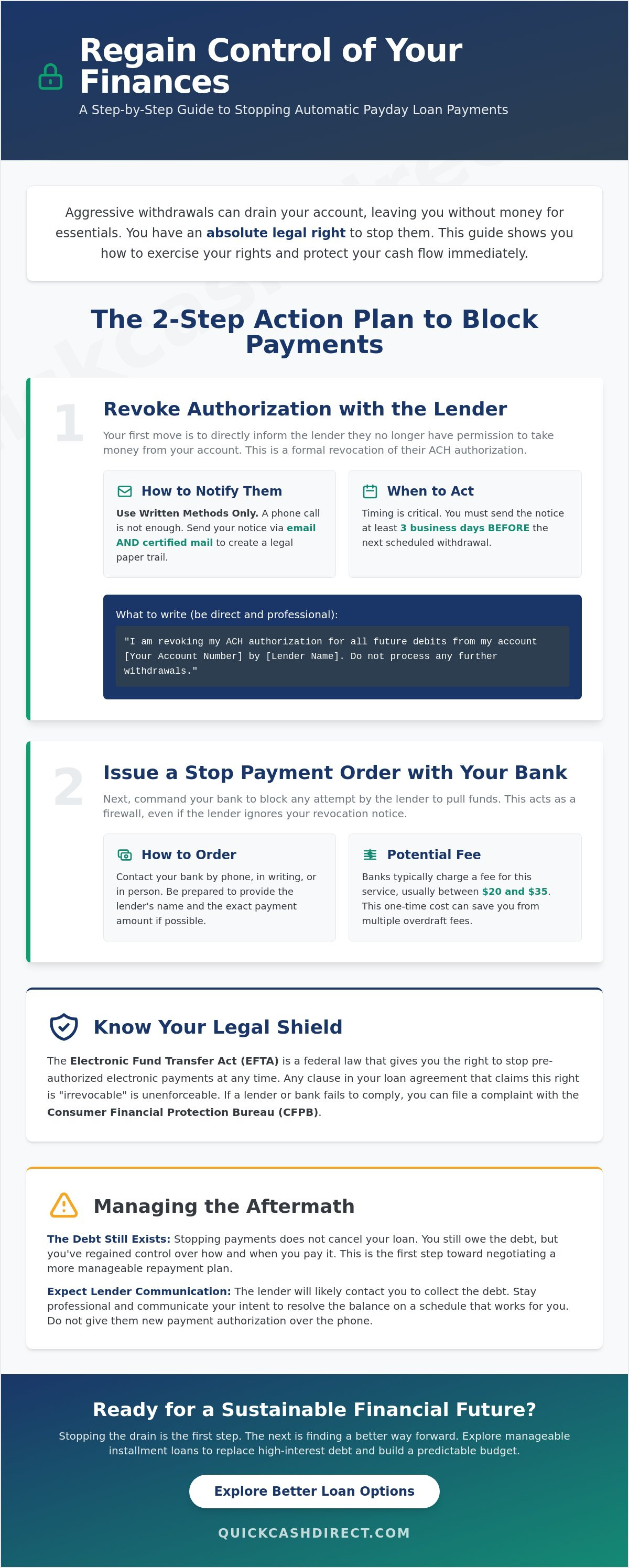

Federal law provides immediate protection for your bank account. You have the legal right to stop recurring electronic fund transfers. This right is absolute. It applies to every consumer in the United States. The Electronic Fund Transfer Act (EFTA) serves as your primary legal shield against unauthorized bank withdrawals. Exercise this right at any time. Do not worry about the fine print in your original loan contract. Contractual clauses that claim you cannot revoke authorization are often unenforceable under federal guidelines.

Understand the distinction between your payment method and your debt. Revoking authorization is not the same as canceling your debt obligation. When stopping automatic payments on a payday loan, you are simply changing how you pay. The Payday loan debt still exists. You still owe the principal and any legal interest. However, you regain control over when and how that money leaves your account. This prevents the lender from taking funds needed for survival. Stopping the "pull" is the first step toward a more manageable financial situation.

ACH Authorization vs. Stop Payment Orders

ACH authorization is the specific permission you gave a lender to "pull" funds from your account. It functions like a digital key to your balance. A stop-payment order is a direct command to your bank to "block" any attempt to use that key. Secure your cash flow by using both methods. Revoke the authorization with the lender first. Then, instruct your bank to block the transaction. This double-layered approach provides maximum security. It ensures your bank stops the transfer even if the lender ignores your request.

The Role of the Consumer Financial Protection Bureau (CFPB)

The CFPB is the federal agency responsible for consumer protection. They enforce the regulations that keep lenders in check. Lenders who ignore your revocation requests violate federal law. The Electronic Fund Transfer Act is the federal law that mandates bank cooperation in stopping these debits. File a formal complaint if a lender continues to attempt withdrawals after you revoke permission. The CFPB uses these complaints to penalize predatory behavior. Stopping automatic payments on a payday loan is a protected action. Your bank must honor your request. Provide notice at least three business days before the scheduled transfer.

Step 1: Revoking Authorization Directly with the Payday Lender

Take control of your finances by cutting off the lender's access at the source. You must notify the lender immediately that you are revoking their permission to debit your account. Do not rely on a phone call. Verbal requests are difficult to prove and often ignored. Send your notice through email and certified mail. This creates a verifiable paper trail that holds the lender accountable. If they attempt a withdrawal after receiving this notice, they are in direct violation of federal law.

Timing is critical for stopping automatic payments on a payday loan. You must act at least three business days before your next scheduled payment date. This window ensures the lender has sufficient time to process the request and stop the transmission to your bank. Understanding What is a payday loan? helps clarify why these lenders prioritize speed in their collections. They rely on the automated nature of the "pull" to secure their funds before you can use them for other needs. Interrupting this process requires a firm, written directive.

Drafting Your Revocation Notice

Keep your communication strictly functional. Your notice must include your full name, your account number, and the specific instruction: "I revoke my ACH authorization for any and all future debits." Do not explain your financial hardship or provide details about your budget. The lender does not need to know why you are stopping the payment; they only need to know that the legal authorization is gone. Save a copy of the sent email. Keep the mailing receipt for the certified letter. These documents are your evidence if you need to file a formal complaint later.

Handling Lender Pushback

Prepare for resistance. Lenders often claim that the original authorization was "irrevocable." This is a common tactic used to intimidate borrowers. Under the Electronic Fund Transfer Act, these claims are usually legally unenforceable. Stay firm. Repeat that you are exercising your federal rights. The lender will likely demand an alternative payment method immediately. If your current debt has become unmanageable, you might consider transitioning to installment loans with more predictable terms. This allows you to address the debt on your own schedule rather than the lender's.

Lenders may also attempt to call you repeatedly once the authorization is revoked. This is a standard collection tactic. You have the right to request that all communication be handled in writing. By moving the conversation to email or mail, you maintain a record of every interaction. This professional distance reduces stress and ensures you aren't pressured into making a verbal agreement that hurts your long-term recovery.

Step 2: Issuing a Stop Payment Order to Your Bank

Contact your bank or credit union immediately after notifying the lender. Revoking authorization with the lender is a legal requirement. Issuing a stop payment order to your bank is your physical defense. This command tells your financial institution to reject any attempt by the lender to withdraw funds. It acts as a safety net if the lender ignores your revocation notice. Accuracy is essential when stopping automatic payments on a payday loan. Provide the bank with the exact name of the lender and the specific dollar amount of the scheduled debit.

Prepare for a small administrative cost. Most financial institutions charge a fee to process these orders. Research indicates that major banks typically charge between $20 and $35 per request. For instance, as of mid-2026, Wells Fargo and WaFd Bank both maintain a $30 fee for stop payment orders on pre-authorized ACH items. While this is an added expense, it is significantly lower than the cost of multiple overdraft fees. You can find more details on how to stop automatic payments through official federal resources. Follow up any verbal order with a written notice within 14 days to ensure the block remains valid under federal law.

Utilizing Mobile Banking for Instant Blocks

Modern banking apps now offer high-speed security features. Open your mobile banking app and search for "Merchant Blocks" or "Stop Payment" tools. These digital features often allow you to halt a transaction instantly. This is faster than waiting for a phone representative. Some institutions categorize these as "temporary" or "permanent" blocks. Select the permanent option when stopping automatic payments on a payday loan. This prevents the lender from simply re-submitting the request under a slightly different name or date. Use these tools to secure your account in seconds.

Confirming the Stop Payment is Active

Verification is the final step in securing your funds. Do not assume the request processed correctly. Check your "Pending Transactions" or the "Stop Payments" list in your online dashboard. Ask your bank for a specific confirmation number. Record this number and the date of the request. This documentation is vital if a payment accidentally clears. Monitor your account balance daily, especially on the day the payment was originally scheduled. Daily monitoring ensures you can react instantly if an unauthorized withdrawal occurs. This proactive approach is the best way to maintain control over your cash flow.

Managing the Fallout: What Happens After You Stop Payments?

Stopping the withdrawal is only the first phase of your recovery. You've protected your immediate cash flow, but the underlying debt obligation remains active. Expect a significant increase in communication from the lender. They will use automated calls, text messages, and emails to demand payment. This is a standard reaction to a revoked authorization. Don't let the volume of messages overwhelm you. You've successfully completed the process of stopping automatic payments on a payday loan, and you're now in a position to negotiate from a place of control.

Address the most common fear immediately: you cannot be arrested for stopping a payment. Debtors' prisons don't exist in the United States. Lenders or collectors may use aggressive language to imply legal consequences, but these are empty threats designed to trigger a panic payment. While a lender can sue you in civil court to recover funds, criminal charges aren't a possibility for defaulting on a high-interest loan. Focus on the facts and ignore the intimidation tactics. Your priority is managing your current cash flow to cover essential needs.

Dealing with Collection Calls

Protect your peace by enforcing the Fair Debt Collection Practices Act (FDCPA). This federal law limits how and when collectors can contact you. If the calls become harassing or interfere with your work, exercise your right to limit communication. Send a formal request stating that they may only contact you in writing. This stops the phone from ringing and ensures every interaction is documented. Keep a detailed log of every message received after you revoked authorization. This log is essential evidence if the lender violates federal regulations or state-specific caps, such as the 36% APR limit in Illinois.

Credit Score Implications

Understand the impact on your credit profile. Most payday lenders don't report your payment history to the three major credit bureaus while the loan is active. However, if you default and the debt is sold to a third-party collection agency, it will likely appear on your report. This can lower your score significantly. Monitor your credit daily using free digital tools available in 2026. If the pressure of high-interest debt is too much, consider applying for emergency loan options that offer more structured repayment terms. This allows you to settle the original debt while maintaining a predictable monthly budget.

The debt will continue to accrue interest and fees according to your contract. In some states, these rates are extreme, with average APRs reaching 652% in Idaho. Stopping the payment prevents an immediate overdraft, but it doesn't stop the balance from growing. Use the breathing room you've gained to evaluate a long-term settlement or a more sustainable loan structure. Your goal is to move from a state of crisis to a state of resolution through efficient, structured action.

Finding Sustainable Financial Relief and Better Loan Options

Take a breath. You've completed the tactical steps of stopping automatic payments on a payday loan. Your immediate cash flow is now secure. However, the original need for funds likely remains. Evaluate why your previous loan became a burden. Single-payment structures often fail because they require the entire principal plus interest back within two weeks. This creates a cycle of dependency. Move toward a more predictable and sustainable debt structure to avoid returning to a state of crisis. Efficiency is now your primary goal.

Seek out financial products designed for flexibility. The 2026 lending market has evolved to offer more transparent alternatives. Industry data shows that the market for lower-APR payday loan alternatives is projected to reach $31.2 billion this year. These options prioritize transparency and structured repayment. By choosing a lender that aligns with your budget, you prevent the need for future stop-payment orders. Focus on resolution, not just temporary relief. Look for lenders that comply with state-specific regulations, such as the 36% APR cap in Illinois or the recent ban on "tips" for app-based lenders in Maryland.

Transitioning to Managed Installment Loans

Replace the payday cycle with fixed payments. Installment loans allow you to break your debt into smaller, predictable chunks over several months. This structure provides the breathing room necessary to manage daily expenses like rent and food. These are effective loans for bad credit because they focus on your current ability to pay rather than just your past mistakes. Fixed terms eliminate the surprise of balloon payments. Secure a schedule that matches your pay dates for maximum efficiency and reduced stress.

How QuickCashDirect Facilitates Fast Funding

Speed is essential in a financial crisis. Our referral process connects you with multiple potential lenders through a single application. This saves time and minimizes friction. You can access direct deposit loans in minutes to cover pressing obligations. We act as a bridge between your current need and a reliable solution. Use our platform to compare rates and find an emergency loan that fits your 2026 budget. Our system prioritizes velocity and security, ensuring you get the funds you need without the predatory terms of the past.

Stay informed about your state's specific regulations to maximize your protection. For example, Washington recently proposed increasing the maximum small loan principal to $1,200. Understanding these shifts helps you choose the right amount and lender for your specific situation. Stopping automatic payments on a payday loan was your first defensive move. Now, take offensive action by securing a loan with manageable terms. Efficiency and clarity are your best tools for long-term financial recovery. Select a partner that values your time and provides a clear path to debt resolution.

Take Control of Your Financial Future Today

You now have the tactical tools to protect your bank account from unauthorized withdrawals. Remember that the Electronic Fund Transfer Act is your permanent legal shield. By stopping automatic payments on a payday loan, you disrupt the cycle of predatory debits and regain immediate control over your cash flow. You've learned how to revoke authorization in writing and use modern banking tools to block future attempts. This defensive strategy is the essential first step toward a more stable financial reality.

Transition from defense to a sustainable solution. Don't let the fallout of a single unmanageable debt derail your long-term progress. Access our national network of lenders to find options for all credit types. Secure a better path with fast funding via direct deposit. Secure a manageable loan that fits your budget today. Take this final step to move from a state of crisis to a state of permanent resolution. You can rebuild your financial health with the right partner and the right information.

Frequently Asked Questions

Can a payday lender sue me if I stop automatic payments?

A payday lender can sue you in civil court to recover the unpaid balance of your loan. They cannot, however, pursue criminal charges or have you arrested for stopping a payment. Civil lawsuits are expensive and time-consuming for lenders, so many prefer to negotiate a settlement or sell the debt to a collection agency instead of going to court.

How much does it cost to stop a payment at a bank in 2026?

Expect to pay between $20 and $35 for a formal stop-payment order at most major financial institutions in 2026. For instance, Wells Fargo and WaFd Bank currently charge a $30 fee for this specific service. While this is an immediate cost, it is a necessary step for stopping automatic payments on a payday loan and avoiding the far higher cost of multiple overdraft fees.

What is the Electronic Fund Transfer Act and how does it help me?

The Electronic Fund Transfer Act (EFTA) is a federal law that establishes the rights and liabilities of consumers in electronic fund transfers. It provides you the legal authority to stop a recurring transfer at any time. Under this act, your bank must honor your request to block a debit as long as you provide notice at least three business days before the transfer occurs.

Will stopping my payday loan payment hurt my credit score?

Stopping a payment does not directly impact your credit score because most payday lenders don't report to the major credit bureaus. Your score will only be affected if the debt remains unpaid and the lender eventually sells the account to a collection agency. Once a collection agency reports the default, you will see a significant drop in your credit rating.

Can I stop a payment if I already signed a contract allowing it?

Yes, you can stop a payment regardless of what your original contract states. Federal law under the EFTA overrides any contractual language that claims your authorization is "irrevocable." You have the absolute right to change your mind and initiate stopping automatic payments on a payday loan at any point during the life of the loan.

What happens if the lender tries to debit my account after I revoked authorization?

Any attempt to withdraw funds after you have revoked authorization is a violation of federal law. Contact your bank immediately to dispute the transaction and recover your money. You should also file a formal complaint with the Consumer Financial Protection Bureau (CFPB) to ensure the lender faces regulatory scrutiny for their unauthorized actions.

Is it better to close my bank account to stop a payday loan?

Closing your bank account is a drastic measure that should be avoided. It can lead to a negative report in the ChexSystems database, making it difficult to open a new account for several years. It's much more efficient to use the legal revocation process and stop-payment orders to protect your funds while keeping your banking history intact.

How do I write a revocation letter to a payday lender?

Draft a short, functional letter that includes your full name, account number, and the current date. State clearly: "I am revoking my ACH authorization for all future debits from my account." Send this notice via email for an instant record and follow up with a certified letter to ensure you have a verifiable paper trail of your request.