What if the fastest way to solve a financial emergency isn't just getting the cash, but knowing exactly what it costs to the penny before you sign? You need immediate relief from urgent bills. The confusion over complex terminology often makes the borrowing process feel overwhelming. It's natural to worry about the hidden costs of short term loans when you're in a rush to secure funding. You deserve a clear, professional path from a state of need to a state of resolution without any unexpected obstacles.

We agree that speed should never come at the expense of transparency. This 2026 guide identifies every potential fee and interest trap before you borrow so you can secure an instant cash loan today with total confidence. We'll show you how to read a full repayment schedule and avoid late fees or rollovers. This overview breaks down the math and the latest regulatory changes to ensure your transition to financial stability is fast, safe, and predictable.

Key Takeaways

- Learn how processing speed and lender risk factors determine your final borrowing cost.

- Identify the specific origination fees and penalty triggers that define the hidden costs of short term loans.

- Compare the single-payment structures of Payday Loans against the sovereign-backed terms of Tribal Loans.

- Follow a simple two-step checklist to calculate your exact "Total of Payments" before you commit.

- Access a vetted network of lenders through a streamlined process designed for maximum transparency.

Understanding the Price of Speed: Why Short-Term Loan Costs Vary

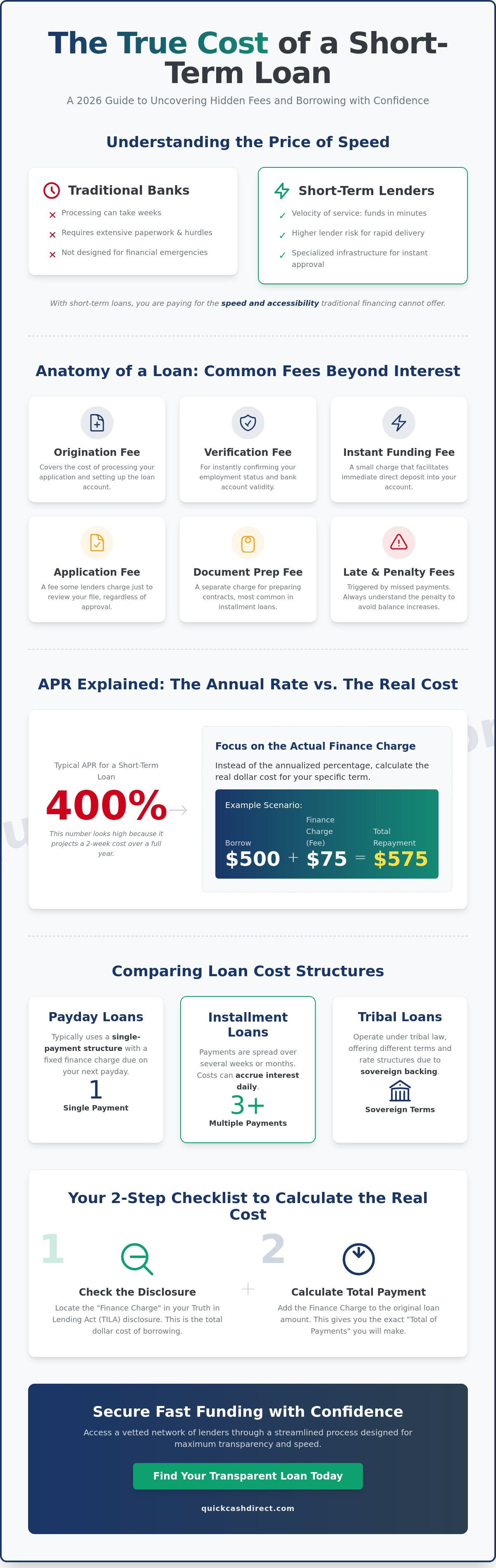

Traditional banks operate on a timeline that doesn't match your emergency. They often require weeks for processing and extensive paperwork. Short-term loans provide essential liquidity when you face immediate financial pressure. This speed is the primary value driver for these products. You aren't just paying for the capital; you're paying for the velocity of the service. Lenders assume higher risk to deliver funds quickly without the hurdles of traditional financing. This risk and the specialized infrastructure required for rapid processing create the specific cost structure you see in your agreement.

Transparency is the mandatory standard for 2026. You must have access to every number before you sign any document. This clarity is your best tool to identify and manage the hidden costs of short term loans. Federal agencies continue to update protections to ensure you stay informed. For example, the Truth in Lending Act (Regulation Z) threshold increased to $73,400 for 2026. This change reflects a broader push for consumer awareness in the lending market. Use this structured information to transform a stressful state of need into a clear state of resolution.

Understand that accessibility has a direct relationship with cost. High-velocity lenders use advanced technology to verify your application in minutes. This allows for direct deposit loans in minutes no credit checks might otherwise delay. When you choose an instant cash loan today, you prioritize immediate resolution. Always confirm the full repayment schedule to ensure the service fits your current requirements. Efficiency and safety are the foundations of a successful borrowing experience.

The Role of APR in Short-Term Lending

The Annual Percentage Rate (APR) is a comprehensive measure of loan cost. It includes interest and most associated fees. For a Payday loan, the APR often appears high. This happens because the calculation projects the cost of a short-term product over an entire year. Don't let the annualized percentage distract you from the actual dollar amount. Focus on the total cost of credit for your specific term. Compare the APR across different lenders to find the most efficient option. Use this metric as a safety marker to verify you're getting a competitive rate for the speed provided.

Fixed Fees vs. Interest Rates

Short-term products often use different cost frameworks. A cash advance usually features a flat finance charge. This is a one-time fee for the service provided. In contrast, some installment loans accrue interest daily. Locate the "finance charge" section in your contract immediately to see the total price. Identifying these hidden costs of short term loans early prevents surprises on your due date. Whether you're looking at tribal loans or standard payday options, knowing if you pay a fixed fee or daily interest helps you plan your repayment accurately. Secure your funding with a clear understanding of these mechanics.

The Anatomy of a Loan: Common Fees Beyond the Interest Rate

Interest rates are only one part of the financial equation. Understanding the full cost of credit requires looking at the specific fees attached to your agreement. This clarity is essential to avoid the hidden costs of short term loans. Lenders often include charges for the administrative work required to provide high-velocity funding. These costs allow for the speed and accessibility you need during a financial crisis. You pay for the infrastructure that makes rapid resolution possible.

Origination fees cover the cost of processing your application and setting up your account. Many lenders also charge verification fees. These cover the digital systems used to confirm your employment status and bank account validity instantly. While these fees are standard, they vary between providers. Always check your contract for instant funding fees. These small charges facilitate the immediate direct deposit access that defines a modern cash advance. If you need a payday loan online, look for these line items before clicking accept.

Administrative and Processing Charges

Application fees are the first potential hurdle. Some lenders charge this just to review your file, regardless of the outcome. You might also see document preparation fees in installment loan contracts. These are separate from the interest rate. You can find these details in your Truth in Lending disclosure. Just as the CFPB explains all the costs associated with a mortgage, your short-term loan contract must list every charge clearly. Check these disclosures to confirm you aren't paying for services you don't need.

Default and Penalty Fees

Late payment penalties impact your balance immediately. Missing a deadline by even one day can trigger significant charges. You must also account for returned payment (NSF) fees. These occur if your bank account has insufficient funds when the lender attempts a withdrawal. In this scenario, both the lender and your bank may charge you. These penalties are avoidable through structured planning and precise timing. Professional lenders prioritize resolution and may offer alternative schedules to keep your account in good standing.

Rollover fees are among the most expensive hidden costs of short term loans. These charges apply when you extend your loan due date instead of paying the balance in full. This creates a cycle that increases your total debt. Avoid these by communicating with your lender early if you anticipate a delay. Proactive communication is a professional safety marker. It helps you maintain a predictable repayment schedule and keeps your path to resolution clear and manageable.

Comparing Cost Structures: Payday, Tribal, and Installment Loans

Every financial emergency requires a specific tool for resolution. You must choose a loan structure that matches your immediate cash flow and your ability to repay. Payday loans and cash advances offer a high-velocity bridge to your next paycheck. These products typically use a single-payment structure. You pay the principal plus a flat finance charge on a fixed date. This model is efficient for small-dollar needs but requires total repayment in one lump sum. Understanding the hidden costs of short term loans in this category means looking closely at that single due date.

Installment loans offer a different path. These products allow you to spread the cost over several months. This distribution reduces the immediate impact on your monthly budget. You pay a portion of the principal and interest with each scheduled payment. This creates a predictable sequence that is easy to manage. Choosing between these structures depends on the urgency of your bill and the duration of your need. Professional transparency ensures you see the total cost of credit for each option before you commit to a plan.

The Unique Mechanics of Tribal Loans

Tribal loans operate under the sovereign authority of federally recognized tribes. This sovereign status means these lenders follow tribal law rather than individual state interest rate caps. While they must still comply with federal laws like the Truth in Lending Act, their fee structures often differ from local options. Use tribal loans when you need specialized funding options that prioritize accessibility. Always evaluate the total cost of credit in the tribal agreement. These lenders provide a vital bridge for borrowers who may not qualify for traditional bank products.

Installment Loans: Predicting Your Monthly Outlay

Predictability is a major advantage of the installment model. These loans distribute interest across the entire term of the agreement. This prevents the sudden financial shock of a single large payment. When you use easy installment loans for bad credit, you secure a fixed repayment schedule. This transparency helps you avoid the hidden costs of short term loans associated with repeated rollovers. Compare the total interest paid over several months against the cost of multiple payday extensions. You will often find that a structured installment plan offers a more stable transition to financial resolution.

Select the loan type that fits your timeline. Use the following criteria to decide:

- Payday Loans: Best for small gaps between paychecks.

- Tribal Loans: Best for high-velocity needs with sovereign-backed terms.

- Installment Loans: Best for larger amounts that require monthly budgeting.

- Cash Advances: Best for immediate, small-dollar emergencies.

The Borrower’s Checklist: How to Calculate the Real Cost of Credit

Speed is essential during a financial crisis, but you must verify the math to ensure a successful resolution. Use the following checklist to eliminate the hidden costs of short term loans before you commit to any agreement. Start by locating the "Total of Payments" amount in your contract. This single figure represents the absolute amount you will repay, including the principal balance and all combined interest and fees. Identifying this number immediately transforms a complex transaction into a predictable sequence. Next, identify the specific date each payment is due. Align these dates with your income schedule to prevent friction and maintain your financial momentum.

Confirm if your agreement includes any early payoff or prepayment penalties. Efficient lenders allow you to settle your balance ahead of schedule to reduce your total interest expense. You should also check for mandatory credit insurance or add-on products that increase your total debt without providing immediate cash. These items often appear in the fine print as optional but recommended services. If you need a fast cash advance, use these steps to verify your agreement instantly. This structured approach ensures you secure the funding you need without any financial surprises.

Reading the Truth in Lending Act (TILA) Disclosure

Federal law requires every lender to provide a TILA disclosure for your protection. This document is your best friend during an emergency because it standardizes how costs are reported. The TILA disclosure acts as your primary shield against hidden costs. It focuses your attention on four key boxes: the APR, the Finance Charge, the Amount Financed, and the Total of Payments. The Finance Charge shows the exact dollar cost of the credit you are receiving. The Amount Financed is the actual cash amount deposited into your account. Review these boxes first to ensure the terms feel reliable and attainable for your current situation.

Red Flags in Loan Agreements

Watch for vague language in any contract you review. Terms like "service charges" or "maintenance fees" that aren't clearly defined are significant red flags. A professional partner will always provide a written fee schedule before you complete your application. If a lender refuses to offer this transparency, it's a signal to look elsewhere. Be especially careful with no credit check loans. These products provide vital accessibility for borrowers with bad credit, but they require extra attention to the fine print to avoid the hidden costs of short term loans. Verify every line item to maintain control over your path to resolution.

Secure Fast Funding: How QuickCashDirect Simplifies Your Search

QuickCashDirect serves as a high-velocity bridge between your immediate financial need and a network of professional lenders. Efficiency is the foundation of our service. We prioritize your time by streamlining the transition from a state of stress to a state of resolution. Our platform is designed for maximum transparency. We ensure you have the tools to identify any hidden costs of short term loans before you accept an offer. By centralizing the search process, we provide a structured path to liquidity that traditional institutions cannot match. You get the clarity you need to make a fast, informed decision.

We specialize in connecting users with direct deposit loans in minutes no credit checks might otherwise delay. This focus on speed ensures you address urgent bills without unnecessary friction. Our system identifies options that fit your specific financial profile. You receive clear, actionable information to help you maintain a predictable repayment schedule. Efficiency and safety are the core value propositions of every interaction on our platform. Secure your funding with a partner that values your time and financial stability.

The Referral Advantage

A referral service provides a significant strategic advantage during a financial emergency. You avoid the high-stress task of hunting for individual cash advance terms on multiple websites. Our 2026 digital matching engine processes your requirements instantly. It delivers a curated list of vetted lenders who are ready to assist you right now. This comparison tool helps you filter out high-fee options and focus on the most competitive offers available. You save time and reduce the risk of encountering hidden costs of short term loans that often appear in less transparent agreements. Use our technology to move through the decision-making process quickly.

Ready to Resolve Your Emergency?

Action is the fastest way to eliminate financial stress. Our 3-minute application process is built for immediate consideration. We use advanced security protocols to protect your data while you shop for the best rates. These recurring safety markers ensure your information remains secure throughout the high-speed narrative of your loan search. You don't have to navigate a complex or multi-clausal process. We deliver a lean, high-velocity experience that mirrors the urgency of your situation. Follow these steps to secure your funding:

- Complete the short, 3-minute digital application.

- Review the vetted offers matched to your profile.

- Verify the Truth in Lending disclosure for each option.

- Select the loan that provides the fastest resolution.

Get your instant cash loan today and take control of your financial schedule. We act as your dependable partner to ensure the path to a result is short, logical, and fully transparent.

Take Control of Your Financial Resolution Now

You now possess the specific knowledge required to identify the hidden costs of short term loans with clinical precision. Use the Truth in Lending Act disclosure as your primary tool for verification. Always confirm the "Total of Payments" to ensure the amount is predictable and manageable. You've learned how to distinguish between flat finance charges and daily interest to select the most efficient structure for your situation. This clarity is the ultimate bridge between a financial problem and a fast, safe solution.

Access our network of 100+ trusted lenders to find terms that fit your profile. Our secure 256-bit encrypted application protects your data while you shop for the best rates. Funds are often available in minutes via direct deposit once you secure an approval. Don't let unexpected bills create lasting stress when a structured path to relief is available. Apply Now for a Transparent Fast Loan and move forward with confidence. Your resolution is just a few clicks away.

Frequently Asked Questions

What are the most common hidden costs of short term loans?

The most frequent additional charges include origination fees, account verification fees, and late payment penalties. These administrative costs cover the specialized technology required for high-velocity processing. Always review the finance charge section of your contract to identify these specific line items. This structured approach ensures you understand the absolute dollar amount required for resolution before you commit to the funding.

Can a lender charge a fee if I pay my loan off early?

Most professional short-term lenders do not charge prepayment penalties. Settling your balance ahead of schedule often reduces the total interest or finance charges you owe. Check the "prepayment" section of your Truth in Lending Act disclosure to confirm your specific terms. Choosing a lender that allows early payoff is an efficient way to minimize the total cost of your credit.

Why is the APR so high on a 2-week payday loan?

The Annual Percentage Rate projects the cost of a short-term product over an entire 365-day year. Because these loans provide liquidity for only 14 to 30 days, the mathematical projection creates a high percentage that doesn't reflect the actual dollar cost. Focus on the total finance charge to understand the price of the service for your specific borrowing period. This helps you identify hidden costs of short term loans that an annualized rate might obscure.

Are there extra fees for receiving a loan via direct deposit?

Some lenders charge an instant funding fee to facilitate immediate direct deposit access. This charge covers the cost of using specialized payment networks to deliver funds in minutes. Standard direct deposit is typically included in the base cost of the loan. Verify if your lender distinguishes between standard delivery and high-velocity "instant" funding to avoid small, unexpected processing charges on your statement.

What happens to the cost of my loan if I miss the due date?

Missing a due date triggers immediate late fees and potential returned payment charges from both the lender and your bank. These penalties increase your balance instantly and can lead to expensive rollover fees if you extend the loan. Proactive communication is your best tool for resolution. Contact your lender before the deadline to discuss alternative schedules and prevent these avoidable costs from accumulating.

Do tribal loans have different hidden costs than standard payday loans?

Tribal loans operate under sovereign authority and may feature different fee structures than state-regulated products. While they must comply with federal disclosure laws, their administrative charges often reflect the unique regulatory environment of sovereign funding. Evaluate the "Total of Payments" in a tribal agreement just as you would with any other loan. This ensures you maintain transparency regardless of the lender's legal jurisdiction.

How can I calculate the total cost of my loan before signing?

Identify the "Total of Payments" box in your federal disclosure document to see the exact amount you will repay. This figure combines the principal, interest, and all mandatory fees into a single, manageable number. Use this amount to verify that the loan fits your budget. This simple calculation is the most effective way to eliminate the hidden costs of short term loans before you finalize the transaction.

Are application fees normal for online short-term loans?

Application fees are common with some providers to cover the cost of credit pulls and file reviews. However, many professional referral networks connect you with lenders without requiring an upfront payment. Confirm the fee structure of the specific lender before you submit your final application. Prioritize lenders who offer clear fee schedules to ensure your path to funding remains fast and predictable.